Sometimes it seems that not a month has gone by without some expert or institution putting out a report on how America’s great Asian rival has become the global leader in dozens of the technologies and products most vital for the future. Or how the rising star’s economic achievements pose a security threat. And then there are the books predicting a war.

Oh, I forgot to say that I’m not referring to comments about China today, but to Japan a few decades ago. I’m not predicting China will also suffer lost decades; what I’m saying is that triumphs in a few leading sectors are poor predictors of overall performance. People often ask which portrait of China is more representative of reality: the one highlighting China’s stunning technological rise or the one stressing its serious macroeconomic travails. Both portraits are true; they’re just not the whole picture. Like Japan before it, China is caught in a “high-technology/low-productivity trap,” as described in a prescient 2020 report by the US International Trade Commission.

Innovation Leadership Does Not Automatically Mean Economic Leadership

Technological innovation by itself does not create growth. Instead, growth happens when companies figure out how to transform innovation into economic value.

That’s why measures of China’s prowess, like the widely cited Global Innovation Index (GII), are terrible predictors of overall economic performance. In 2013, China ranked 35th in GII. By 2025, it had reached 10th, surpassing Germany, Japan, France, and Israel. Among other upper-middle-income countries, the next-highest was Malaysia, in 34th place. So, China’s progress is absolutely remarkable.

But GII has its limits as a predictor of overall economic performance. Yes, as poor countries become richer, improvement in GII scores is part of the recipe. However, once countries become rich, it’s not so simple. On the contrary, among the top twenty countries in 2025, there was no correlation between their GII ranking and growth rates. Consequently, in a prescient comment, the ITC wrote in 2020 that “China’s own growth rate and productivity gains have been declining even as its GII rankings have risen.”

Superstar Sectors Are Tiny Share of China’s “Dual Economy”

Like Japan in the 1980s, China suffers from a “dual economy,” a hybrid of super-productive, export-oriented sectors that dazzle the world and an even larger mass of domestically oriented, low-productivity sectors that hamstring the economy. Japanese and Western policymakers focus mostly on the impressive parts of the economy because those are the ones impacting their countries.

Among China’s big superstars are electric vehicles, solar energy, and batteries. Global demand for these products is growing exponentially, and China is beating everyone else in filling that demand. Yet only 1.5% of Chinese workers produce solar energy products and components. Only 0.7% work in making all autos and auto parts, not just EVs. And only 0.2% make batteries.

Moreover, there’s a large gap in productivity (GDP per worker) across sectors. Manufacturing has the highest efficiency, although there are big differences among subsectors. In 2024, factories employed 18% of all Chinese workers but produced 25% of GDP. By contrast, 22% of Chinese labored in farming, but they produced only 7% of GDP. If we count factory productivity as 100, then farming stands at 22, whole/retail trade at 47, and construction at 72. Yet, these lagging sectors add up to almost half (45%) of all jobs.

The Best And The Rest

While some Chinese companies in certain sectors have made remarkable technological achievements—e.g., solid-state batteries—these advances are not being diffused to typical companies in the same sector.

A World Bank Report, Firm Foundations of Growth, showed this divergence between the best and the rest was already a problem during 1998-2007, when China was doing so well. The 10% most productive manufacturing companies employed 33% of the factory labor force but accounted for 60% of productivity growth within firms. By contrast, the bottom 70% employed almost 40% of factory workers but accounted for only 15% of within-firm productivity growth.

Undoubtedly, this divergence between the best and the rest has worsened over the past 15 years, as the economy has grown more sluggish. And it’s likely even worse outside of manufacturing. Unfortunately, reliable data on this issue are not available for the recent period.

Refusal To Cull the Zombies

Worse yet, as in Japan, huge numbers of zombie companies are being sustained on artificial life support. That denies resources of labor, capital, finance, and real estate from those who could use those resources better and, as a result, drags down growth.

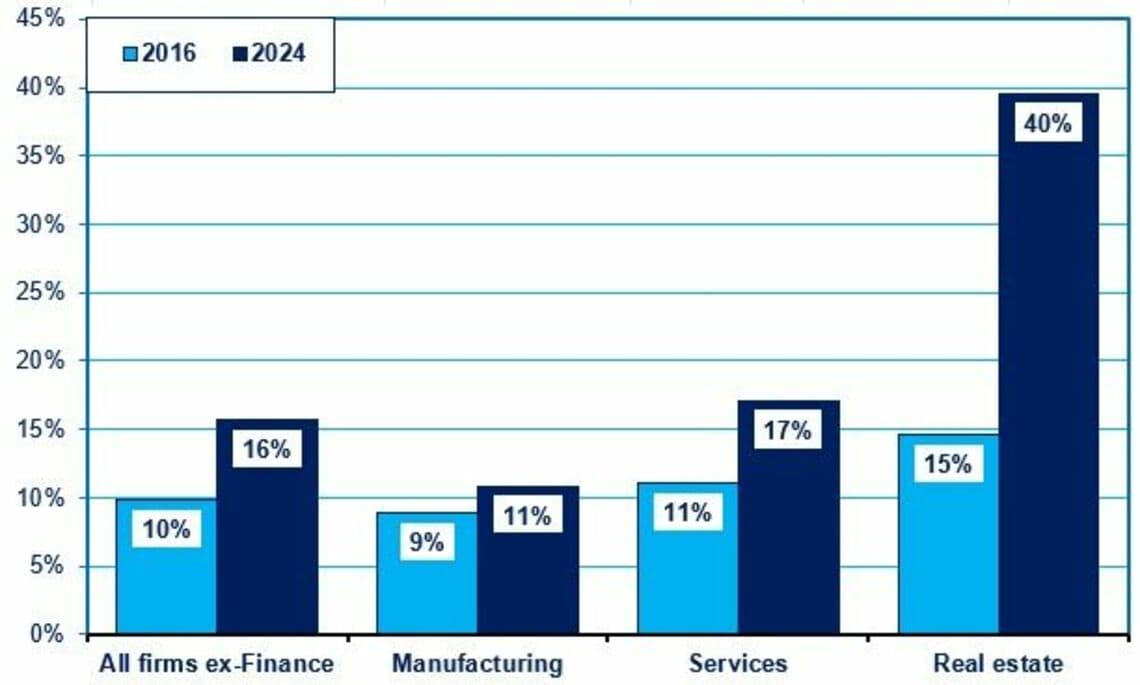

Share of Zombie Copmanies in China

Consider China’s auto sector. Alongside China’s world-beating companies like BYD, Geely, Cherry, and a dozen others, there are about 230 hapless enterprises. Almost 100 of them sell fewer than 10,000 units per year. As a result, China has the capacity to produce twice as many autos as it can sell at home or abroad. This has resulted in a price war that hurts the best companies. China has wasted a lot of investment on factories that create virtually no GDP. Such overcapacity is seen in many industries. China tries to flood the world with exports from the sectors plagued by overcapacity.

With every passing year, we see a rise in the share of firms in China that cannot earn enough even to pay their interest bill. Economists at the Dallas Federal Reserve Bank reported that the share of manufacturing assets held by zombie firms has risen from 4% in 2020 to 11% in 2024. In services, half of GDP, the zombie share of assets has reached 17%.

Stalled Entry Of New Firms

All economies require the entry of new, more innovative firms that replace older, less productive companies. It is the economic equivalent of nature’s survival of the fittest. Not surprisingly, then, in the period up to 2007-2008, two-thirds of China’s remarkable growth of manufacturing productivity came from the entry of new companies.

Unfortunately, the entry of new firms and their share of factory jobs peaked around 2007 and then declined sharply through 2013. The job share fell from 25% in 2007 to 15% in 2013 in the digitally intensive sectors, and from 20% to 10% in the rest of manufacturing. The share has undoubtedly declined even further since then. It’s no coincidence that, as the entry of new firms slowed, so did productivity growth.

China Investing More Instead of Investing Better

Like Japan, China is trying to boost labor productivity by piling on more and more investment. But as economies mature, investment faces diminishing returns.

I saw in Yunnan Province how building modern roads replaced subsistence farming with market-oriented farming, thereby greatly improving both productivity and farmers' incomes. But, at some point, it takes far more renminbi of road-building to gain each additional renminbi of GDP growth. While giving workers more computers boosts their productivity, it helps even more to replace a 2010 computer with one made in 2026. China’s obsession with excessive investment, rather than helping more companies learn to exploit better technology, is a main reason China now struggles. Japan makes the same mistake.

Total Factor Productivity (TFP) is the yardstick that captures the benefits of such upgrades. It involves not just technology in the narrow sense, but how well firms use that innovation. In the long term, countries need healthy TFP, not just lots of investment, to grow well.

From 1980—the beginning of Deng Xiaoping’s reform—through 2009, growth in GDP per worker accelerated to a stunning 9.3% per year, and a third of this leap came from growth in TFP. But as the years passed, the pace of TFP growth increasingly decelerated. Finally, according to the World Bank, TFP growth was negative in every year from 2013 through 2022 (the latest available year).

If China is in trouble, it is the result of Xi Jinping's decision to reverse many of the policies that created the Chinese miracle. Rather than face these flaws, Beijing has made it a violation of national security law to “defame” the economy by pointing out its shortcomings.