Even before the Iran war, the Bank of Japan faced a big “stagflation dilemma” affecting the timing of the BOJ’s next rate hike. The war has not only worsened that dilemma but made the future far more uncertain. Hence, instead of raising rates this month, forecasters believe it will happen in April, June, or July. This depends on how long the war lasts and what tremors it unleashes.

The stagflation dilemma is that steps to curb inflation further slow an already stagnant economy—GDP is barely higher than in 2018—while steps to buoy the real economy worsen inflation. Since the BOJ says its decisions will be data-driven, let’s look at the signals the data are sending to the central bank.

By the way, the two BOJ Policy Board members that Prime Minister Takaichi appointed replaced two other “doves.” There is no increase in the number of those opposed to early rate hikes.

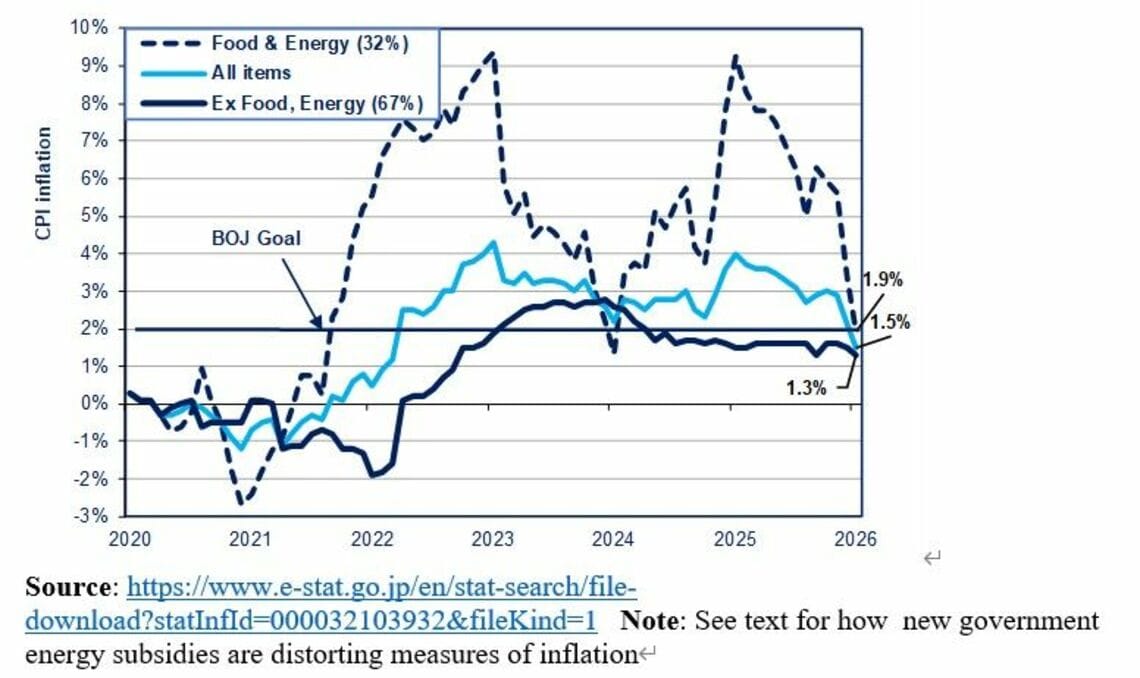

Inflation: Headline Too High While Real Core Is Too Low

Let’s start by looking at January’s inflation data. Keep in mind that big subsidies for gasoline, electricity, and natural gas substantially lowered the picture for overall inflation. However, it did not affect the picture for food or for core inflation, which excludes all food and energy.

Firstly, inflation excluding food and energy fell further to just 1.3%, even further away from the BOJ’s 2% goal. It has been steadily moving in the wrong direction for the past two years .

This category is most important because, being less volatile, it is a better indicator of medium-term inflation trends and the best leading indicator of progress toward a healthy 2% inflation driven by domestic demand. The numbers belie the BOJ’s confidence in its January 2026 “Outlook Report” that, “underlying CPI inflation…will increase gradually and, in the second half of the projection period [2007 through March 2028] be at a level that is generally consistent with the price stability target [of 2%],” a year later than it had forecast in its January 2025 report. The BOJ has a terrible track record on predicting inflation since it feels bound to claim its policies are working.

The energy subsidies were put in place to placate voters whose living standards are determined not by core inflation but by overall inflation. For the same reason, Takaichi promises a two-year suspension of the consumption tax. The subsidies are so big that they sent headline inflation plunging from 2.1% in December to 1.5% in January. They lowered energy inflation from negative 3.1% in December to negative 5.2% in January.

With oil prices predicted to hit $100 a barrel fairly soon, this will reverse. Currently, the subsidies are set for January through March. They could be extended. Food inflation meanwhile remains at 4%. With food comprising 26% of the household budget, that’s a big deal.

The upshot is that unhealthy cost-push inflation is telling the BOJ to raise rates now while core inflation is telling it to wait.

Disappointing Wage Hikes Are Telling BOJ To Delay Raising Rates

The reason why core inflation is only 1.3% is that wages remain far below the 3% annual growth the BOJ says is required to reach 2% inflation. In January, nominal wages rose only 2.4%, and the three-month average was just 2.2% .

Low wages lead to lower consumer spending. How can Japan enjoy a healthy level of demand-led inflation if domestic demand is so stagnant?

The BOJ often points to the spring “shunto” wage negotiations between companies and unionized workers as a good leading indicator. But only 16% of the labor force, mostly at bigger companies, is covered by these negotiations. The high nominal wage hikes in the 2024 and 2025 shunto deals did not spread to the general workforce.

The BOJ often finds fault with the series in the chart above because it does not sample the same workers each month. It prefers a survey that examines the same workers every month. But this survey shows that, after briefly touching 3% in 2004, wage hikes have decelerated. They were just 2.1% in January. The upshot: wages are telling the BOJ to delay raising rates.

Stable Interest Rates and Yen/$ Make Life Easier for BOJ

Back in December and January, alarmists started tossing around talk of Takaichi’s “Liz Truss moment” because of a temporary upward blip in the 10-year JGBs, and a big jump in thinly-traded 30-year and 40-year JGBs. Sure enough, interest rates have come back down. Before the Iran war, they were below the 2024-26 trend line, and right now they are just about equal to it. If this pattern holds despite the war, the BOJ need not fear investor panic forcing its hand.

Bond investors were encouraged by Takaichi’s overwhelming victory because they felt Takaichi had less need to add more fiscal stimulus than she wanted in order to gain opposition votes in the Diet. But they may be underestimating the degree to which her favorite economic guru wants her to open the fiscal spigot.

I’ve heard reports that a few economists at major banks in Japan are worried that overseas investors will eventually stop buying JGBs due to fears of Takaichi’s fiscal expansionism. That’s important because foreigners now own 12% of all JGBs and short-term bills, and accounted for a bit more than half of the net buying of them in 2025. Moreover, foreign investors have been net buyers of JGBs for the six months through January (the latest data).

Yes, the financial press makes much of relatively small changes in rates because they have a huge impact on traders in JGBs and interest rate derivatives. But the changes are too small to make much of a difference to the real economy.

The same is true of the yen’s value. Recent fluctuations of the ¥/$ rate before and after the beginning of the Iran war have stayed well within the trading range that has prevailed since October.

Had the yen dipped a great deal, that would have put pressure on the BOJ to raise rates sooner rather than later. No one knows what the yen’s value will be in two or four weeks. For now, however, the BOJ can breathe a little easier on that front.

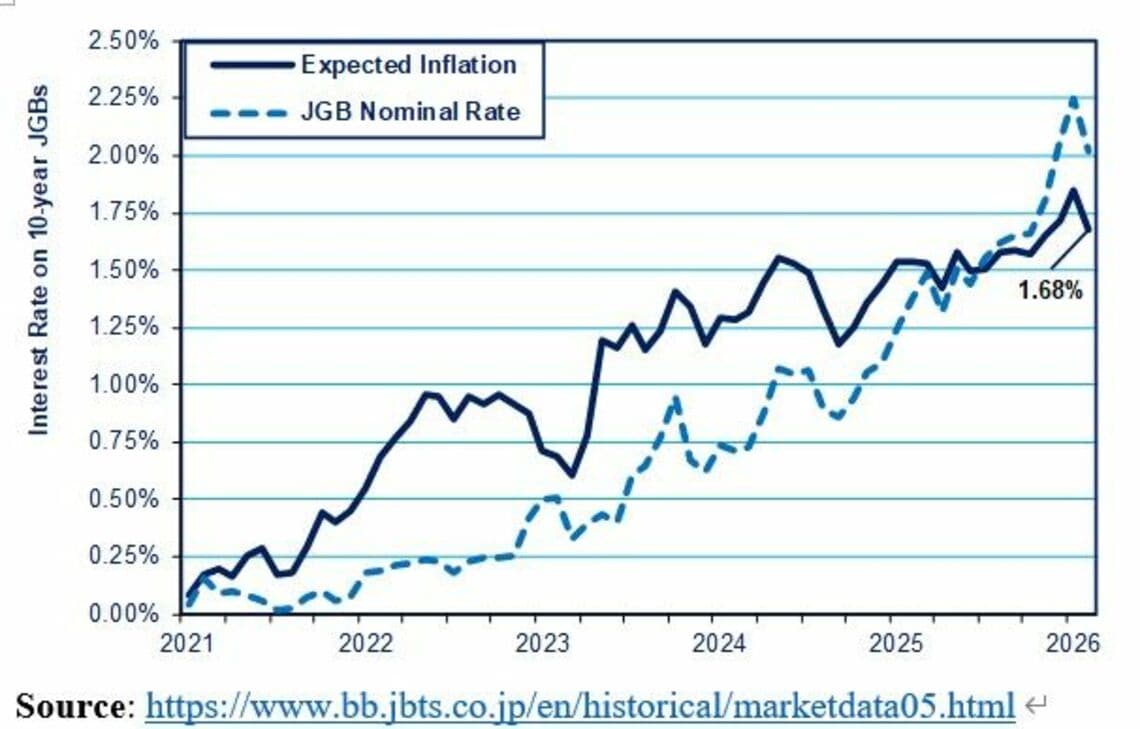

Inflation-Index JGBs Show No Panic On Inflation or Interest Rate Spike

The so-called “breakeven rate of inflation” on inflation-indexed ten-year JGBs—the JGBi— is also telling the BOJ that it need not rush to hike interest rates.

The so-called breakeven rate is a forecast of the inflation that investors expect over the coming year. If its forecast is correct, these bonds earn the same “real” interest rate as regular JGBs. If inflation is lower, they make more money; if it’s higher, they make less. As of the end of February, the expected inflation rate over the next 10 years was just 1.68%.

The gap between the breakeven rate and the interest rate on regular bonds tells us the real rate of interest that investors anticipate. The real rate has risen as Japan moved to inflation. It spent many years in negative territory. That’s because the interest rate on normal JGBs cannot go below zero (except for a tiny amount).

If prices are falling 1% per year, then the real rate is negative 1%. As of Feb. 27th, the real rate was a mere 0.35%. That’s because the slack economy means that the demand for credit is weak relative to the supply. Even Takaichi’s need for more JGB issuance is not big enough to change that basic picture .

One caveat: the volume of such bonds is much higher than that of similar bonds in the US and Europe, and thus a less reliable indicator of investor sentiment. However, because Japan has moved from deflation to inflation, the volume is growing.

Forecasters See BOJ Raising Overnight Rates to 1.5-to-2% by 2027 or 2028

This market perception is harmonious with the view of the BOJ. The Bank believes the “neutral rate of interest”—i.e., an overnight interest rate that neither accelerates nor depresses GDP growth—is somewhere between slightly negative and slightly positive. Given its inflation target of 2%, the Bank says that the current overnight rate of 0.75% is substantially below the neutral rate. So, the Bank views itself not as tightening monetary policy but as gradually normalizing rates to bring them to neutral.

BOJ Governor Kazuo Ueda has refused to be pinned down on where that neutral rate would be, saying that estimates range from just 1% to 2.25%. Economists at financial institutions expect the BOJ to raise the overnight rate to around 1.5% or 1.75%, believing that Japan needs a slightly negative interest rate. Takaichi’s economic guru, Takuji Aida, sees the BOJ raising the overnight rate to around 2% by 2028, believing 0% is the neutral interest rate.