Japan faces a trade war launched by its two biggest customers. China is escalating its restrictions on exports to Japan over Taiwan issues. Meanwhile, even though the US Supreme Court ruled that Donald Trump’s tariffs are illegal, Trump has threatened higher tariffs on Japan and others if they try to reduce the 15% tariffs they previously agreed to under that threat. China and the US together buy almost two-fifths of Japan’s global shipments.

Tokyo’s main strategy is to diversify its export destinations to lessen Japan’s dependence on either China or the US. It wants to increase Japan’s role in Free Trade Agreements, such as luring the European Union into joining the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP). The UK has already joined. At the same time, it is trying to placate Trump, lest he impose even harsher measures against the auto industry, its main priority. For example, Tokyo has said it will stick to the 15% tariff and the $550 billion investment package. It only asked Washington that Japan not be made worse off than before.

Diversification may sound good, but it's not so easy to accomplish in a world of globally integrated supply chains. How much Japan sells to China and the rest of Asia depends on their own sales to the US. Together, the US, China, and the rest of Asia account for almost three-quarters of Japan’s exports. If the US buys less from China and the rest of Asia, Japan will sell less to them.

While diversification and FTAs are necessary, they are woefully insufficient. Japan has to make its internal economy more resilient, so it is less vulnerable to external economic shocks. I’ll discuss how to do that at the end.

Many people presume Japan’s exports to China depend mainly on the growth of China’s internal market as well as its global exports. In reality, the more important factor is how much China exports to the US. Moreover, Japan’s exports to the rest of Asia also depend on China’s exports to the US.

The reasons are twofold. Firstly, the kind of products that Japan exports to China and the rest of Asia tend to serve as inputs to products made in China, whose final market is rich countries. Think of Japanese chips in iPhones assembled in China. Secondly, today’s international supply chains are highly interconnected. The production of many electronic products requires the participation of dozens of countries.

There are, of course, exports to Asia that do not depend on links with China, such as vehicles and auto parts. However, Japan is losing market share in autos, mostly to emerging Chinese challengers.

China’s exports to the US have been declining as a share of China’s total exports since 2018, and in absolute numbers since 2021 and partly, this is because China and the US have each been trying to reduce their dependence on the other. The Trump trade war is accelerating this trend, with Chinese exports to the US in during April-September 2025 down a whopping 35% from the same period of 2022. A closer look at the trade linkages shows why this is hurting Japan.

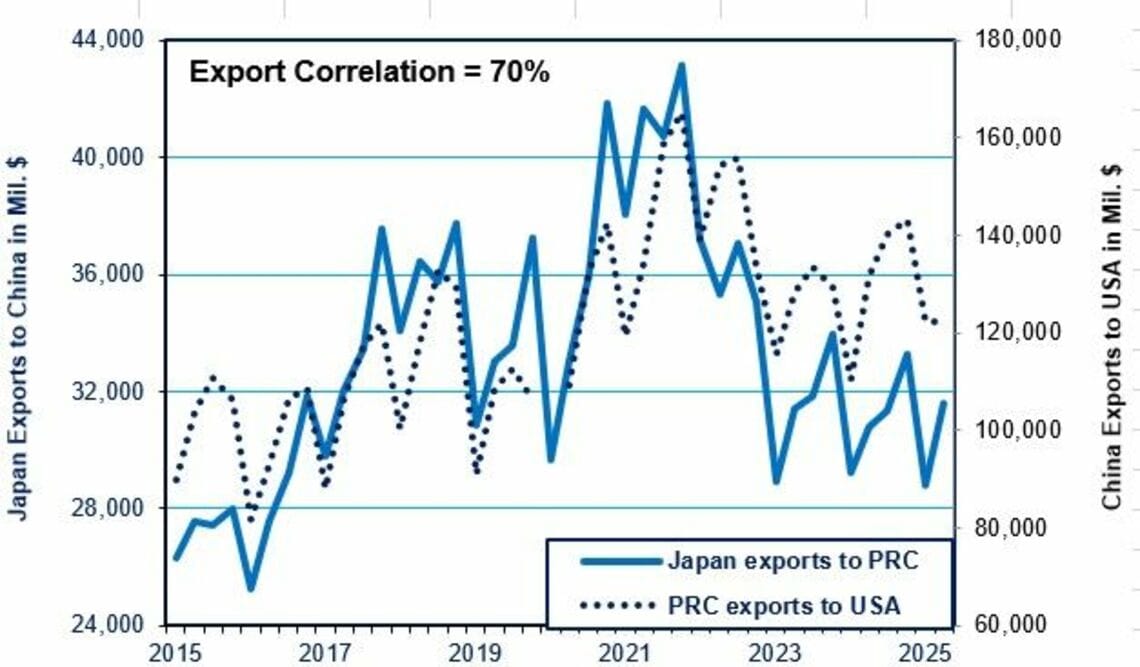

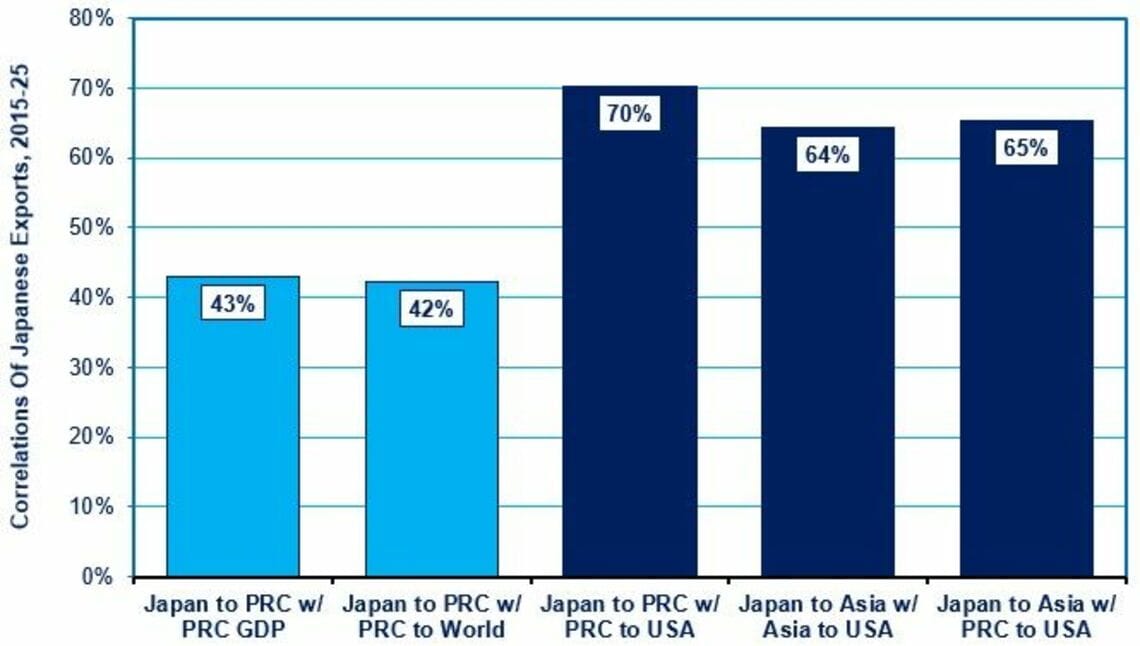

The dark blue column in the middle of the chart below shows a high 70% correlation between Japan’s exports to China and the latter’s exports to the US. By contrast, the two light blue columns on the left show a much lower correlation between Japan’s exports to China and either China’s internal growth in GDP (just 43%) or its global exports (just 42%).

There’s a similar pattern when we look at the emerging Asian economies (excluding rich countries such as Korea, Taiwan, Hong Kong, and Singapore), there’s a 64% correlation between Japan’s exports to them and their own exports to the US (second column from the right). But the truly amazing dependence is the following: Japan’s exports to emerging Asia hinge on China’s exports to the US, with a 65% correlation (rightmost column). In short, there is a tightly integrated quadrilateral supply chain: Japan exports inputs to Asia, which incorporates them in its own exports to China, and then China uses these in its exports to the US.

Similarly, Japan’s exports to Korea depend very much on Korea’s exports to China, which in turn depend on China’s exports to the US. Japan’s exports to Taiwan also hinge on China’s exports to the US.

Trump neither knows nor cares about the havoc he is wreaking on trade networks that took decades to develop and that bring down costs for companies and consumers around the world, including the US. Even if the next President tries to reverse Trump’s damage, it’s a lot easier to turn an aquarium into fish soup than to transform fish soup back into an aquarium.

What Makes Japan Vulnerable to Trump Trade War

Japan suffers from a stop-go economy is highly sensitive to external demand shocks. Over the past three decades Japan has alternated between five-to-six years of growth and five-to-six years of virtually zero growth. The downturns have often big triggered, or exacerbated by external events, such as the Asian financial crisis in the late 1990s, the 2008-09 Great Recession due to the financial meltdown caused by criminal use of financial derivatives in the US and Europe, and the current stagflation triggered by Covid and the Russian invasion of Ukraine.

To make Japan more resilient, policymakers have to examine why Japan is so sensitive to external shocks. The main reason is that consumer demand is so weak. GDP today is only slightly higher than it was in 2018 and that’s because falling real wages have hindered consumer spending. During the decade from 2015 to 2025, household spending provided only 3% of the entire growth in GDP.

Consequently, the government had to make up for the shortfall. Government spending fueled almost 60% of GDP growth. While it looks like business investment was also a big contributor, at 40% of growth, firms were building capacity mainly to serve foreign markets rather than domestic ones. A statistical regression shows that 83% of the growth in investment was oriented towards exports. So, if the trade wars soften exports, business investment will also soften.

Unfortunately, Japan enters the current period with merchandise exports already weak. In 2024, they were only a bit higher than in 2018. All the growth in exports has been in the often-disparaged service sector.

Japan’s exports to China have been flat in yen terms since 2021 and in 2025, shipments to China the lowest share of Japan’s total exports since 2008. Meanwhile, exports to the US have been falling 8% year-on-year in yen terms since Trump announced his tariffs last April.

What Should Japan Do?

Up to now, Tokyo has refused to coordinate with other countries to deal with the Trump trade war, even though some senior officials believe it should. I agree with the latter group. However, the Takaichi administration, like its predecessors, thinks Japan is better off going it alone and letting Prime Minister Sanae Takaichi practice the same sort of “charm offensive” with Trump that they believe helped Shinzo Abe. Tokyo’s priority is the auto industry, and they fear an enraged Trump could punish it. Nonetheless, auto exports to the US in 2025 were 9% lower than in 2023.

In addition to whatever moves Tokyo makes on trade, it is essential to make the economy more resilient internally in the face of external shocks. That, in turn, requires beefing up consumer demand by hiking wages. On this matter, Tokyo is mostly talk, little action.

Low wages subsidize low-productivity companies. When wages rise, especially in countries with flexible labor markets, inefficient firms downsize, or even close, causing labor and sales to shift to higher-productivity enterprises that can afford these higher wages. Sweden successfully used a high-wage strategy to move the country up the technological ladder and, even with higher wages, enjoys low long-term unemployment for native-born workers. Japan should do the same.

Instead of doing this, Japan has tried to use an increasingly weaker yen to keep low-productivity exporters afloat. Anong the 587 manufacturing exporters listed on the stock market, the average company used to be able to export at a profit even with the yen valued at ¥100. By contrast, in 2024, they needed a yen as weak as ¥127. One-sixth of those exporters needed an even weaker yen: ¥150 to ¥155. The 16,000 exporters not on the stock market probably need an even weaker yen.

And Trump’s tariffs have likely pushed the breakeven yen rate even weaker. Higher wages would force a shift in Japan’s exports to the most competitive companies. Conversely, a weak yen raises the prices on food and energy, thereby hurting Japanese household income and spending.

The government has tools to push wages upward.

The single most successful tool has been raising the minimum wage by around 3% per year, to reach ¥1,118 at present. That has lifted 20 million workers out of poverty or near-poverty wage levels. Takaichi’s two predecessors suggested a new target of ¥1,500. In November, Takaichi dismissed that goal as unrealistic, saying it was “hard to set a numerical target for minimum wage now.

The government’s job is to create the environment that allows firms to offer pay that exceeds the pace of inflation.” To help win the election, she shifted to promising a “realistic” hike this summer. But who knows what she considers realistic? Tokyo should aim for 3% growth in real wages until it reaches the ¥1,500 target (in 2025 yen).

Secondly, Tokyo should enforce existing laws mandating “equal pay for equal work” between regular and non-regular workers and between men and between. That would raise wages for those now being discriminated against. France enforces its laws and there is little wage gap between regulars and no-regulars for workers in the same occupation. No agency of the Japanese government even investigates unequal wages.

Instead, the Takaichi administration claims a flood of fiscal stimulus and low interest rates will create a “high-pressure” economy, and this will automatically force wages up. If that were true, how come it has not worked in the past 30 years?

There is no reason for Japan to believe it has few options beside placating Trump and shifting away from China. With the right steps, it can determine its own future.